Ivanhoe Mines Ltd. — Institutional Update (USD, January 2026 UPDATE)

Ivanhoe’s trendline shows incremental fundamental improvement and early market recognition of asset quality. While valuation has not fully caught up to NAV strength.

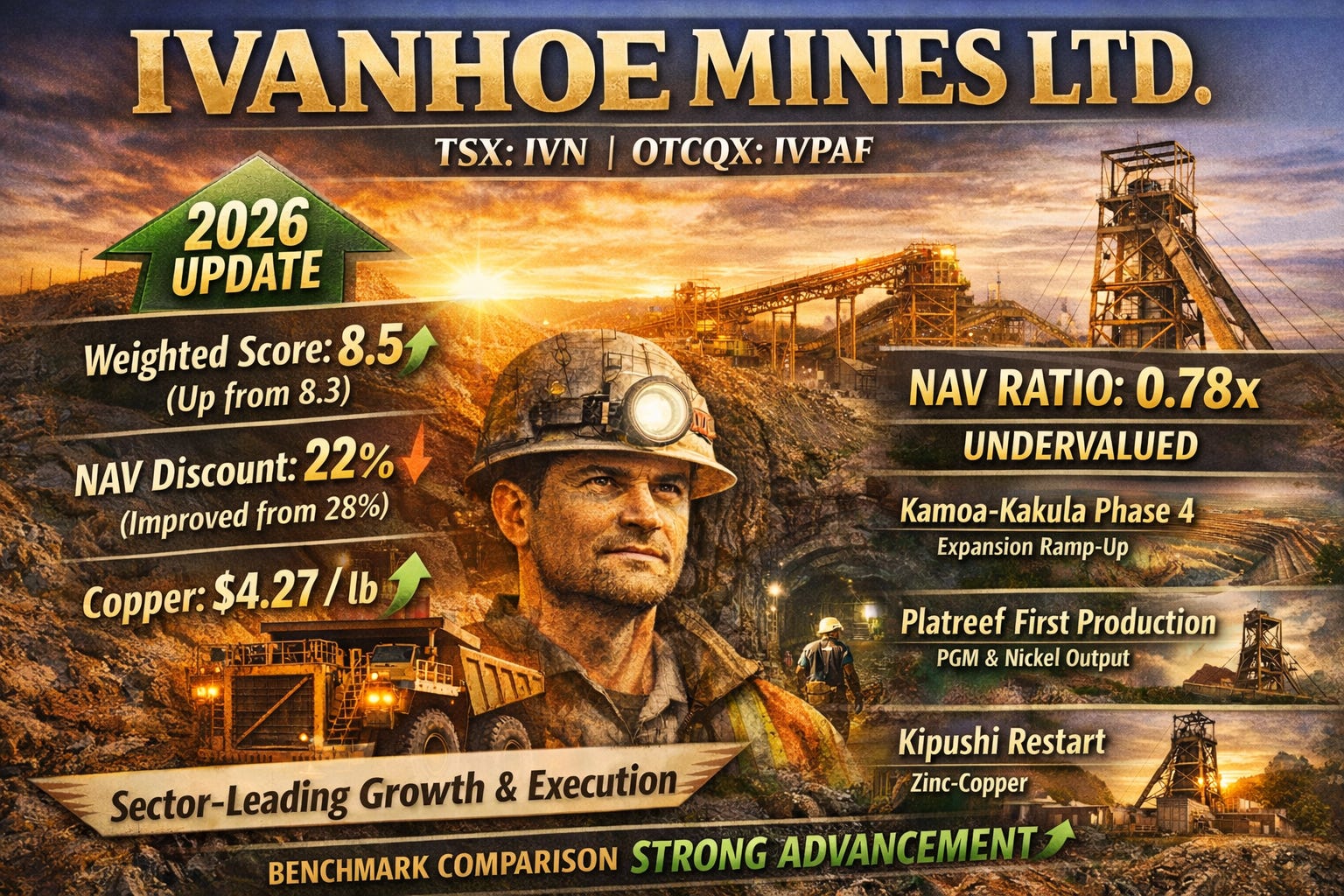

⚙️ Ivanhoe Mines Ltd. — Institutional Update (USD, January 2026)

Framework: Weighted–NAV 7.9.3 (Verified Closing + Ratio Integration + Expanded Thesis Build)

Valuation Date: 2026-01-26

Market Cap: US $18.4 billion

Benchmark Reference: Previous Ivanhoe Mines Report — Mining Stock Analyst (OCT 2025)

1. Executive Summary — Expanded Institutional Thesis

Ivanhoe Mines continues to consolidate its position as one of the sector’s most strategically advantaged growth producers. The company’s three-pillar asset base (Kamoa-Kakula, Platreef, and Kipushi) provides long-duration production visibility across critical metals themes that support global electrification and infrastructure demand.

Management’s track record for phased execution, financing discipline, and technical delivery has attracted continued institutional confidence even amid periodic DRC and South African operational headwinds.

Looking ahead, Ivanhoe’s catalyst stack is weighted toward self-funded expansion and ramp-up events that can convert NAV discount into sustained valuation re-rating.

2. Commodity Price & Market Context

• Copper — $4.27/lb (Kitco verified close) 🟢

• Gold — $5 086.10/oz (FOREXCOM verified close) 🟢

• Silver — $112.29/oz (FOREXCOM verified close) 🟢

• Platinum — $2 722.77/oz (SAXO verified close) 🟢

Commentary: Global refined-copper inventory levels remain below historical averages while energy-transition policies amplify structural demand. Gold and PGM prices at multi-year highs reinforce investor risk hedging and support revenue diversification for multi-metal producers like Ivanhoe. Overall metal pricing trends provide a tailwind to NAV expansion and strengthen sector sentiment entering 2026.

3. Company Overview

• Ticker: IVN (TSX) | IVPAF (OTCQX)

• Market Cap: US $18.4 billion

• Primary Commodity: Copper (≈ 80 % NAV weight)

• Secondary Exposure: Platinum and Nickel (Platreef)

• Flagship Assets: Kamoa-Kakula (40 % JV, DRC); Platreef (64 %, South Africa); Kipushi (68 %, DRC).

Investor Commentary: Ivanhoe operates within two resource-rich but infrastructure-challenged jurisdictions. The company has successfully navigated these environments through strong local partnerships and predictable ESG engagement, reducing execution risk compared to historical peers. Its hybrid copper-PGM profile also provides a natural hedge between industrial and precious metals cycles.

4. Core Analysis

• Management Quality – 9/10 🟢 – Veteran leadership team with consistent delivery on complex project schedules and capital control.

• Geology & Resource Profile – 9/10 🟢 – Exceptional grade, scale, and expandability offer multi-decade production visibility.

• Operations & Efficiency – 7/10 🟡 – Rising energy costs and power constraints in the DRC modestly impact operating margins.

• Balance Sheet Integrity – 8/10 🟢 – Low debt, ample cash, and phased capex reduce refinancing risk.

Commentary: Operational discipline and project sequencing remain Ivanhoe’s defining strengths. The company’s ability to scale output while preserving unit economics underpins its institutional premium. Short-term power and logistics issues are manageable relative to the structural quality of its ore bodies.

5. Risk-Adjusted Metrics & Exposures

• Jurisdictional Risk – 6/10 🟡 – Permitting and infrastructure in the DRC and South Africa remain non-trivial variables.

• Operational Risk – 8/10 🟢 – Decentralized project management and redundant systems support continuity under stress.

• Financial Risk – 8/10 🟢 – Balance sheet strength enables internal funding of growth phases without excess dilution.

Commentary: While sovereign risk is persistent, Ivanhoe’s track record suggests it can operate profitably in complex jurisdictions. Access to international financing channels and joint-venture structures further de-risk development timelines. Investors assign a discount for location, but fundamental execution remains solid.